Sustainability in Practice – Advanced

The course covers in detail the most central topics to know when talking about sustainability, such as sustainable supply chain management, ESG performance reporting, measurement and reference standards, regulatory updates, sustainability reports and the NFS, and product or process certifications.

The course is structured in 9 modules, video-recorded and available in streaming on the Circularity Platform.

The entire course or individual modules can be purchased by credit card or bank transfer and followed in streaming on our platform.

Once purchased, they remain valid for 100 days.

At the end of each module, you can take a quiz to test your level of learning.

At the end of the course, a personalized certificate of attendance will be issued.

The price of the course is to be considered VAT included.

Purchase by credit card or bank transfer

Assessment quiz available at the end of the course

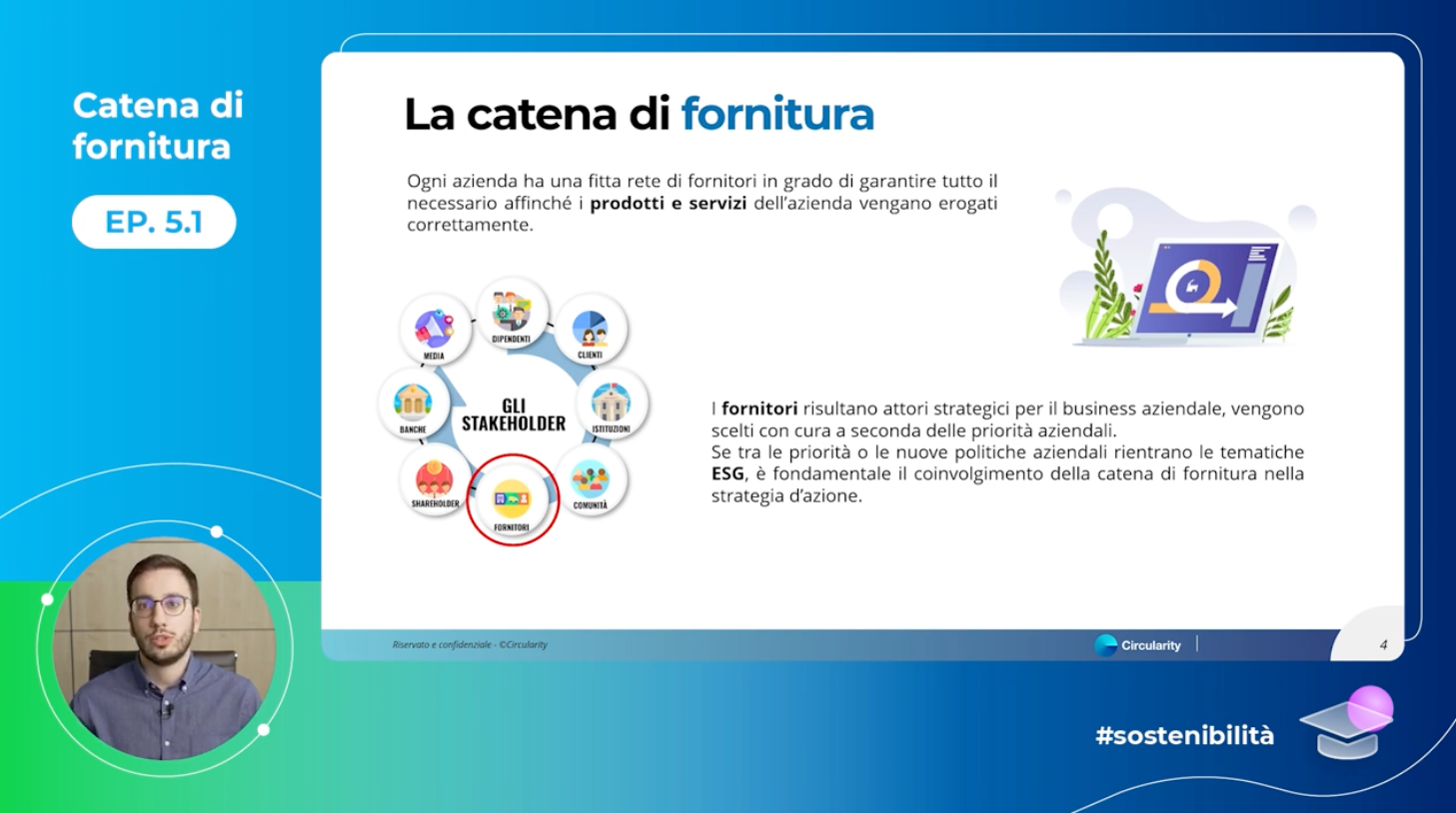

Watch a free preview of the first video of Module 5

“ESG risks arising from the supply chain”

Our Teachers

Master’s degree in Environmental and Territorial Engineering, specialising in Environmental Remediation Technologies, from the Politecnico di Milano; qualified as a professional engineer, with a view to enhancing managerial and professional skills in current sustainability issues. Executive Master’s degree in Circular Economy Management from LUISS Business School. Specialises in sustainability, optimising waste management and treatment, and the principles and application of Green and Circular Economy in specific sector-based projects and within individual companies. Head of training on sustainability and the circular economy, with specific teaching roles on professional Master’s programmes at the Catholic University of Milan, 24Ore Business School and directly within companies through bespoke training programmes.

Having always been keenly interested in sustainability issues and eager to contribute actively to them, he began his professional career as a member of Circularity’s technical team, working as a Sustainability & Carbon Footprint Specialist.

He specialises in the analysis of environmental data within the context of sustainability reporting projects and in conducting carbon footprint studies. Finally, he delivers training courses on sustainability and the circular economy, both as part of professional Master’s programmes at the 24Ore Business School and the Catholic University, and directly to companies through dedicated training programmes.